WE OFFER FULL SERVICE & DO-IT-YOURSELF

|

FULL SERVICE STARTS WITH A FREE CREDIT ASSESSMENT, $1 CREDIT REPORT AND A FREE CONSULTATION

|

|

DO-IT-YOURSELF CREDIT MONITORING $24.99/MO

|

Credit Repair & Financial Coaching Isn't Simply "Another Expense"

It's An Investment In Your Financial Future

Enroll in Credit Repair & Financial Coaching TODAY

Develop Good Financial Habits for a LIFETIME

PHASE 1: Follow These Proven Strategies Throughout Your Credit Repair Process

1) COMMIT TO INVESTING 6-9 MONTHS TO IMPROVE YOUR FINANCIAL FUTURE

- Some credit bureaus may report changes to your credit scores within 30, 60 or 90 days

- However, the recommended time frame to get proven results is usually 6-9 months

- Since bad credit normally develops over a period of time, repairing bad credit also takes time

- Federal and state laws provide credit bureaus and third parties adequate time to investigate and reply to all disputes

- These laws protect consumers and lenders, therefore we cannot offer a "quick fix" program

- Our overall goals are better credit scores, higher approval limits and lower interest rates

- We will empower you to make financial decisions with confidence

- There are two different types of inquiries, often referred to as "hard" inquiries and "soft" inquiries

- Hard inquiries are applications for new credit and they remain on a person's credit report for 2 years

- Hard inquiries lower a person's credit score until a good payment history is established for the new account that was opened

- Soft inquiries review your credit report without extending credit and they remain on a person's credit report for 1 year

- Soft inquiries do not affect your credit score since they are usually for pre-approval offers, employment background checks, insurance quotes, rental applications, credit reviews by companies that you already have accounts with and reviewing your own credit report

- Freezing your account with each credit bureau will prevent your credit score from being affected by new inquiries while we're repairing your credit

- Credit monitoring is a powerful financial tool that provides monthly credit score changes, identity theft protection and other benefits

- FICO score or VantageScore will be recommended based on the financial goals that are shared during your FREE consultation

- A FICO score is usually required for major purchases including mortgages and autos (select the monthly subscription OR 7 day trial for $1)

- VantageScore is available for overall financial health and is usually sufficient for other types of financial goals (select the 7 day trial for $1)

- Credit monitoring is billed separately by the service provider ($25-$35/month) and is required to be maintained during credit repair

- The information from your credit monitoring service allows us to prepare your initial Credit Audit and Analysis

- It also provides monthly updates from the 3 major credit bureaus with the changes to your lender accounts and your credit scores

- A 3-Bureau credit report helps identify discrepancies, incorrect information, fraudulent transactions and potential cases of identity theft

- After you have completed our program, credit monitoring is also an important tool for maintaining your overall financial health on a long-term basis

- Lenders like to see at least 2-3 open credit cards with low balances, an installment loan and a mortgage, and a good payment history for 2 years

- Pay on time by the due date every month by setting up automatic payments

- Pay by the statement date (instead of the due date) to report a lower outstanding balance to the credit bureaus

- Missed payments that are LESS than 30 days past due won't be reported to the credit bureaus, however they could decrease your approved limit

- Missed payments that are MORE than 30 days past due are always reported to the credit bureaus, which can dramatically lower your credit score by up to 110 points and undo the progress that we're making

- Start with the credit card with the highest interest rate and pay it down to 25%, then work on the card with the next highest interest rate until all of your cards are down to 25%

- When all of them are at 25% or less, the credit bureaus will increase your score, resulting in lower interest rates WITHOUT paying off your balances in full

- Then start paying them down IN FULL using the reduced interest rates that are available

- Call any credit card company that doesn't automatically reduce your interest rate and they will usually extend one after reviewing your updated credit history

- Get the best of both worlds with debt reduction AND a sense of accomplishment

- Continue using your open credit card accounts wisely so that they'll be reported as "good" credit

- If you're no longer using a credit card on a regular basis, start using it to pay expenses that you normally pay directly from your checking account or use it to make small purchases from time to time, then set it up to be automatically paid in full each month

- This contributes to a healthy utilization ratio, which is 30% of your credit score

- Paying off an installment loan early may save you interest, provided that there's no prepayment penalty

- However this could negatively impact your payment history, length of credit and types of credit used (credit mix)

- Therefore your credit score would most likely decrease for a short time

- Since you're working towards a higher credit score, continue making your regular monthly payments until your credit repair process has been completed

- Many lenders have temporary hardship relief programs for unemployment, unexpected medical expenses, divorce or other documented circumstances

- A hardship program can pause your payments, lower your monthly payments and/or offer you a lower interest rate

- This allows you to stay current on your account without damaging your credit score

- The duration of the agreement depends on the severity of your hardship and the terms that are offered

- Contact each of your lenders if any of these situations apply to you

CLIENT #1

|

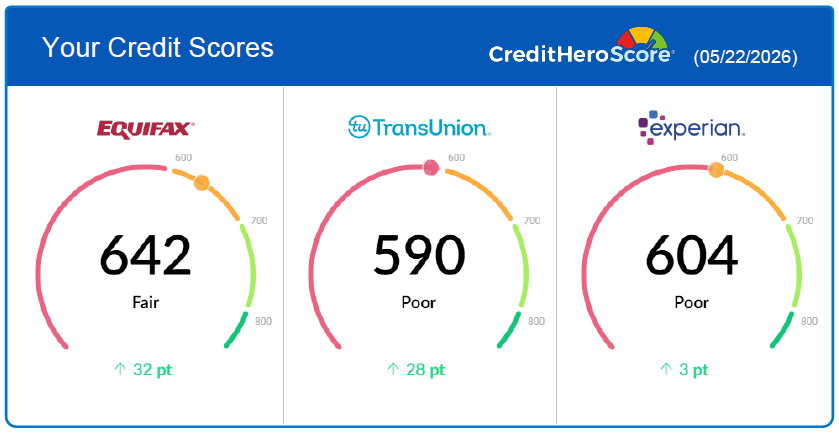

***SCORE INCREASES***

|

CLIENT #3

|

9) STOP APPLYING FOR NEW ACCOUNTS DURING CREDIT REPAIR

- The accounts that are included in your Credit Audit & Analysis Report are the "baseline" for comparison purposes

- Opening new accounts or having new inquiries may lower your credit score for up to a year and reverse the progress that we're making on your behalf

- If opening a new account appears to be a good strategy for you, we'll let you know at the appropriate time

- Please be patient until our credit repair process has been completed

- Existing accounts that are in good standing contribute to a better credit score

- Closing an account that has a positive credit history could lower your score and reverse the progress that we're making on your behalf

- The balance owed on a credit card vs. the approved credit limit is referred to as the utilization ratio

- Credit bureaus calculate higher scores when utilization is below 30%

- If you have high balances, pay them down to 25% or less

- When your balance is low, improve your utilization ratio by requesting a credit line increase and avoid spending more than 25%

- Even if you pay in full every month, if you spend more than 25%, during the month, make additional payments to ensure that your balance stays below 25% at all times

- A collection account may be sold to one collection agency after another, be removed from your credit report and then be reported again

- If you pay off a medical collection, it will be removed from your credit report

- However, other types of paid and unpaid collection accounts can remain on your credit report for up to 7 years

- BEFORE SENDING YOUR PAYMENT FOR A NON-MEDICAL COLLECTION ACCOUNT Request a "pay to delete" agreement IN WRITING from the collection agency to ensure that the account will be removed, otherwise it can remain on your credit report for up to 7 years

- Accounts can be deleted from your credit report if they aren't being reported in compliance with federal and state consumer laws

- However, a creditor may still try to sue you in court, garnish your wages or take other action to collect the amount owed

- If an unpaid debt is deleted from your credit report, it may still be reported for mortgages, government loans and other types of lending

- When applying for financing, sometimes these accounts will need to be paid in full before a new loan can be approved

Credit Repair Tips

Enroll in credit repair & financial coaching

today is the best time |

Develop good financial habits

that will last for a lifetime |

Implement more than one strategy

to get faster results |